Is there a surprise brewing with the X-date?

Total Treasury Model mid June update

Most folks (including myself over the past 5 months) have been projecting an X-date in mid to late August, which translates to a need for Congress to pass some version of the OBBB prior to the August recess (or cancel the recess). Recent data, however, indicates this may not be correct. More on that later in the post but first a recap of where we are.

Lowest TGA in June

The TGA had a closing balance on 6/12 of 261b, close to the 272b the TTM projected it would close at from the last update. This is likely the lowest the TGA will go until the end of July. As of 6/12, Treasury also has ~157b in additional borrowing room (via remaining extraordinary measures), 75b of which it will use today to absorb the net coupon issuance that will settle. Add in the mid June quarterly tax flows (corporate and self employed/retired) and a large one time extraordinary measure that becomes available on June 30th and Treasury should be able to keep the TGA between 300-400b until August.

TTM Performance since the last update

The TGA projection and Debt issuance/redemption projection components of the TTM have performed great since the May 23rd update.

TTM projected TGA Deposits from 5/23 - 6/12: 274.8b

Actual TGA Deposits from 5/23 - 6/12: 277.2b (+2.4b over projected)

TTM projected TGA Withdrawals from 5/23 - 6/12: 449.6b

Actual TGA Withdrawals from 5/23 - 6/12: 457.6b (+8b over projected)

Thus, the TTM under projected the deficit over the timespan by ~5.6b, not bad at all over a 3 week timespan.

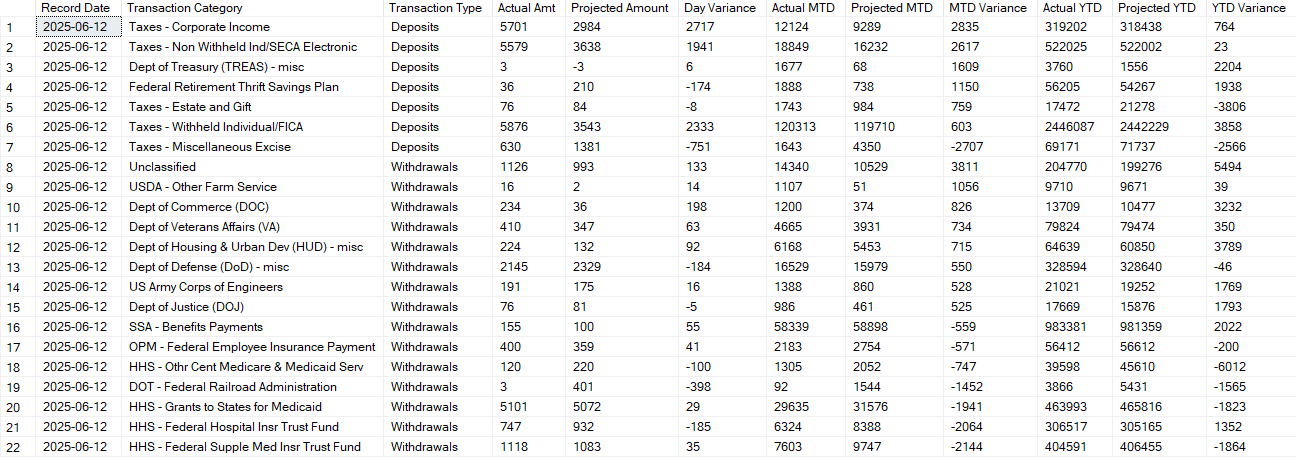

The category internals have been decent as well in June with only 6 categories varying from actuals by more than 2b through June 12th.

None of these category variances are large enough to compel me to tweak any of the individuals category projection models at this time. Also notably, the category for tariffs is not on the list so the tweaks I put in at the end of last month seem to have a handle on tariffs at least in the short term. I will reassess at the end of June.

Bill issuance

In the last update I projected that Treasury would lower the bill amounts on the short tenors again in the week following that updates release, and that indeed happened almost exactly as I projected.

Treasury should be done with the downward adjustments for a while. What drives the downward adjustments (and was also driving the two 10b cash management buybacks over the past couple of weeks that Barchart so breathlessly reported on) is Treasury’s need to stay at the debt ceiling.

If you want a refresher on debt ceiling mechanics see here:

Reverse Engineering the Debt Ceiling

I do not know when Congress will raise or suspend the debt ceiling or what the contours of that eventual deal will look like. What I do know, is they have plenty of time to strike that deal. Unlike 2023, the X-date will not be in June but rather in August. I currently project it to be August 21st. but any date from the 15th on looks vulnerable

Treasury stays more or less right at the debt ceiling by keeping a cushion of extraordinary measure room (primarily in the G Fund) to “absorb” net positive coupon issuance on the days that spikes on the mid month and end of month settlement days. Take today (6/16) for example. Treasury will have net coupon issuance of ~75b. They MUST stay at the debt ceiling so as to not violate the law, so they will redeem 75b of the 137b in the G fund, issue an IOU that doesn’t count towards the debt ceiling and offset the 75b in net new coupons. Treasury does this dance with the G Fund every day, balancing not just net coupon (and bill) issuance but also changes in various other large government trust funds (social security etc.) Anticipating this large need today, Treasury “built up” the G Fund balance over the past few weeks by reducing bill issuance (resulting in negative bill issuance) and those cash management buybacks.

The end of June coupon settlements will require ~140b in extraordinary measure room, so you might think that Treasury would keep decreasing the bill issuance to create enough room. Fortunately for Treasury though, there is a one time extraordinary measure in the Civil Servicer Retirement Fund, which totals ~130b in additional room, which will simplify Treasury’s life by becoming available on June 30th as well which will provide Treasury the room it needs to absorb the net coupon issuance without needing much from the G Fund.

The TTM includes a detailed modelling of flows into and out of the government trust funds which is a core part of understanding when the precise X-Date will be. It is included in the “Combined Views” tab of the TTM Model Output in the spreadsheet at the end of this post and separately broken out on the “Extraordinary Measures” tab. Its the most challenging aspect to model but the TTM does a fairly decent job with it.

Going forward I actually have one week of upwards adjustment (10b a piece) to short tenor bill issuance modeled at the beginning of July, along with a sizable cash management bill (65b) from the beginning of July until right before the end to keep most of the additional room provided by the extraordinary measures in the TGA since I assume while Treasury cannot keep it at the normal risk policy level they would like to keep it as high as possible. Treasury may choose a different pattern (e.g. multiple weeks of short tenor bill increases in late June/early July instead of a split of bill increases and a cash management bill) but the broader point is, Treasury has extraordinary measures room to work with over the next month and a half and I doubt they will just let it sit.

Withholding Tracker

Withholding made the variance list above, but just barely at 603m more that I was projecting through June 12th. Bottom line, it is coming in pretty much exactly as I the model expects in June, so no slowdown in this datapoint from my models algorithmic perspective. I honestly expect to see one, but the data and algorithm are what they are and they just dont right now, See the late May update for more detail on the projection methodology for this category.

X-Date Impact

This is where it gets a little interesting.