Why QT will taper, even if the Fed leaves it alone

Why QT will taper, even if the Fed leaves it alone

Plus February 24 QT projections

TLDR

QT will reduce Fed balance sheet by ~75.8b in February: 60b for UST, 15.8b for MBS. UST coupon reduction is very slightly heavier on the mid month vs. end of month maturities. No bill rolloff this month.

UST QT will “taper” this year even if the Fed does nothing due to a quirk in how the rolloff mechanics play out.

Greetings!

At some point this year the Fed is likely to announce an explicit plan to taper QT, which will almost certainly involve the lowering of the monthly rolloff caps for UST, currently at 60b. The MBS cap likely wont get lowered but with prepayment rates still only generating 15-20b in rolloff a month, the Fed could lower the MBS cap substantially and not affect the actual rate of balance sheet reduction. But Im not breaking any news here. This is pretty widely known and expected.

The Mechanical Taper

What isn’t widely known, unless you were a keen reader of my post last August ( https://johncomiskey.substack.com/p/treasury-issuance-is-what-really) is that UST QT will fail to hit caps in June, September, and December in 2024, instead only rolling off 48.2b, 34.6b, and 30.1b in UST those months. So rolloff will “taper” even if the Fed leaves the caps alone, and the effect will be even more pronounced in 2025.

Why does this happen? Its due to a quirky intersection of the rolloff/reinvestment mechanics and the issuance/maturity schedule of some coupon UST. The root issue is that in general, fewer coupon UST mature in March, June, September, and December. Why is that the case? Because the longer tenor coupons (10yr/20yr/30yr) as well as Floating Rate Notes and TIPS don’t mature every month. They issue every month, but don’t mature every month. The longer tenor coupons have a new issue every February, May, August, and November (if you are thinking hey that’s when the Quarterly Refunding Announcements are, that’s no coincidence). In the two months following a new issue, that new issue is “reopened” to add more to it. So if you bought a new 10yr note in November it would mature in 10yr, but if you bought a reopened 10yr note in December, it would mature in 9 years and 11 months, in January 9 years and 10 months. The net effect is that while there are new 10yr (or 9yr 11 month or 9yr 10 months) notes being auctioned and issued every month, 10 yr notes only mature four times a year in February, May, August, and November. Same for the 20yr and 30yr bonds. FRNS issue new/mature in October, January, April, July and TIPS issue new/mature in January, February, April, July, and October (with reopenings in other months). Notably missing are the months of March, June, September, and December.

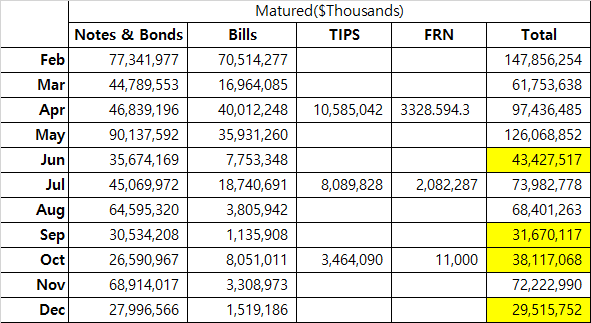

Only the shorter dated coupon tenors (2/3/5/7) mature in March, June, September, and December. Accordingly, since QT ramped up to 60b in UST rolloff a month back in September of 2022, those months have been much more likely to have less than 60b in coupons maturing and thus have to rolloff bills those months to hit the 60b cap. Sure fine John, but there are still ~210b in bills held on the SOMA, plenty enough to continue to cover the difference right? Well it would be if the bills in the SOMA and when they mature were evenly distributed across the months, but they aren’t now. They have become very lopsided such that in 2024, very few bills at all will be maturing in the months June, September, and December. There wont be a ton in March either, but it will be just enough for the Fed to not miss cap. Borrowing a table put together by @yang_youngbin, you can see where things stand presently

Note how many fewer bills are slated to mature in March and June versus the surrounding months. You can even see the effect in September and December though most of the bills that will mature after July have yet to be issued.

Why is this imbalance happening. Again, mechanical quirks related to the tenors of bills. Two of the benchmark tenors, the 13 week and 26 week bills, have maturities that stay contained within the same the same set of four calendar months. For example, 13w and 26w bills issued in February will very likely mature in May and August. If the Fed reinvests those maturing bills into new bills in May and August, which they will because as we discussed above coupons will be above the 60b cap because of the maturing 10/20/30s, then the new 13w and 26w bills purchased in May and August will very likely mature in August/November and November/February. So they mostly get “stuck” in those four months. The 13/26s “stuck” in March/June/September/December have been being steadily depleted since the beginning of QT and are about to be more or less gone after March.

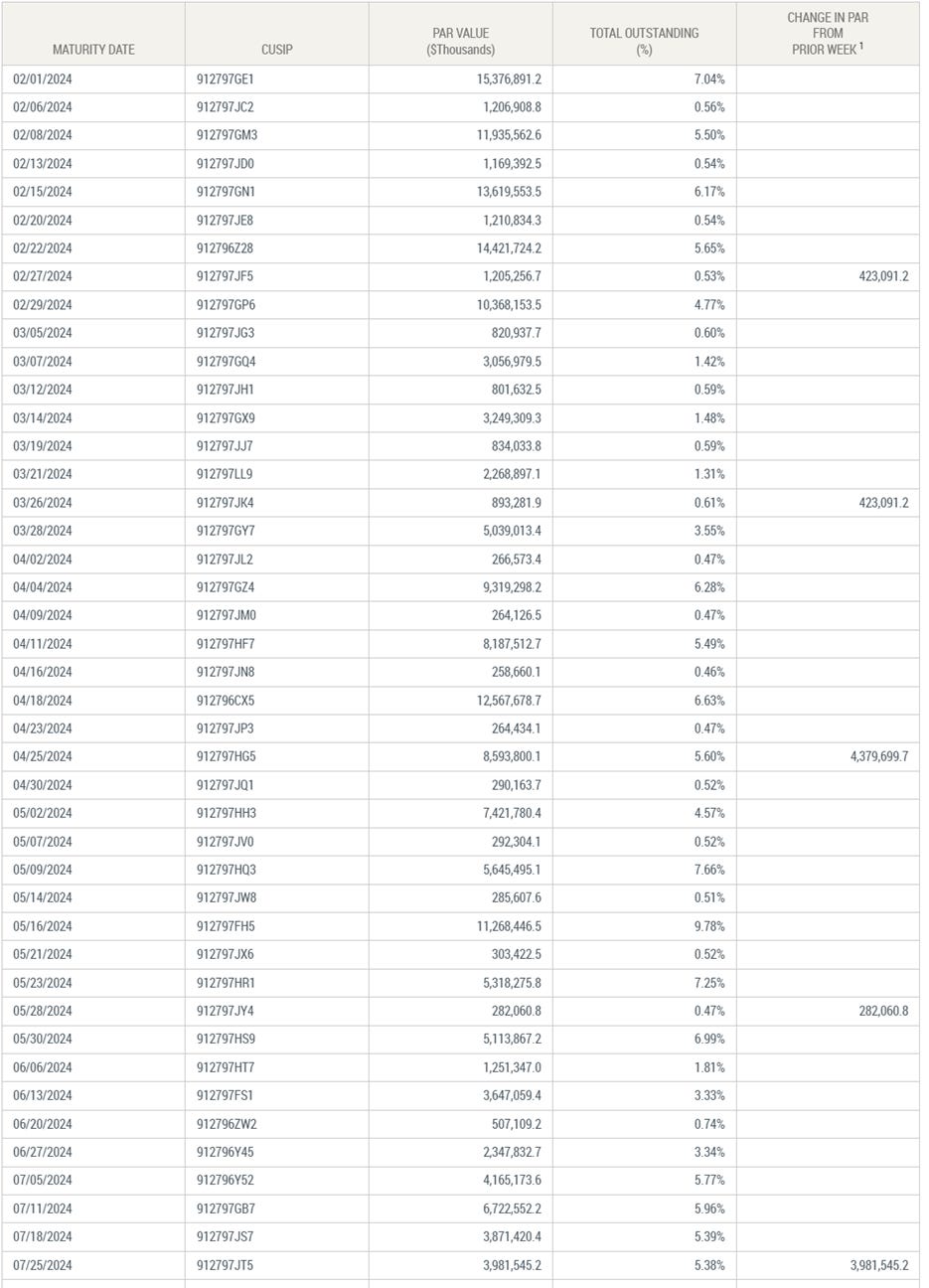

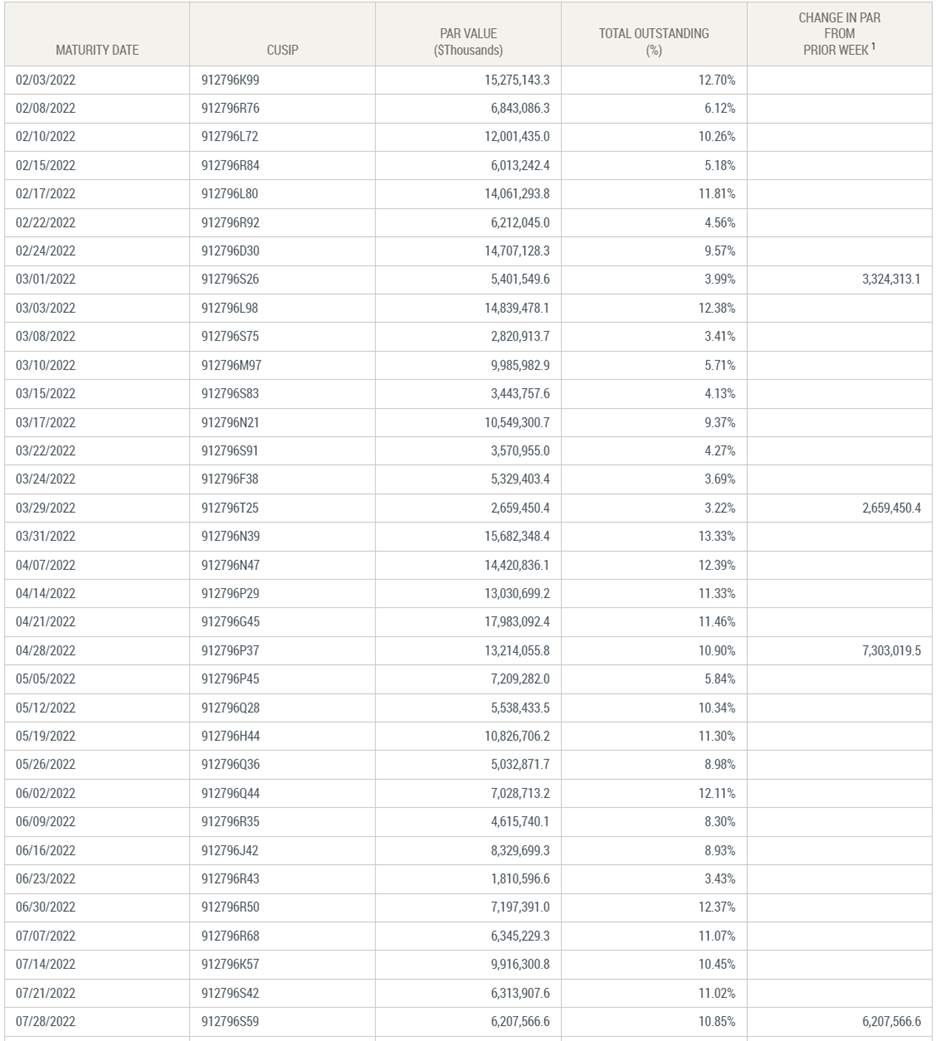

What about the 4w/8w/17w? Shouldn’t those tenors not get trapped in the same four months? Yes but there are very few of them left in the Fed portfolio. Compare this readout of the bills in the SOMA versus those bills in 2022

Bills in the SOMA circa Feb 2022

Note how much more skewed it is to Thursday maturities (13/26w bills) versus Tuesday maturities since 2022. This is mostly because the Fed reinvests what is maturing in bills proportionally into what is issuing that same day, so the Tuesday/Thursday cadence gets stuck too. Thus when bills rolloff in March, June, September, and December it not only starves that four month cadence of the 13w/26w bills in that cadence, but it also drains 4w/8w/17w across all the months resulting in SOMA bill holdings that are almost entirely concentrated in 13/26w bills that mature in the months outside of March, June, September and December.

Could the Fed choose to alter the rollover/reinvestment mechanics for bills? Absolutely they could, but these mechanics have been around for a while (predates this QT cycle) and Im a firm believer that inertia is one of, if not the most powerful organization force in the universe (particularly the government) so I don’t think they will just to make sure there are enough bills to hit cap in June/Sept/Dec/March going forward.

On the other hand, one force that rivals inertia in power is the fear of public embarrassment. Remember when Chair Powell struggled to explain the late settling MBS and why the balance sheet was still rising in the very early days of QT? Perhaps he will want to avoid having to potentially explain why UST isn’t hitting the caps in June. If so, stepping down the UST cap to 45b in June and then 30b in September would neatly sidestep having to explain why UST wasn’t hitting the 60b cap in June/September/December/March, at least until September 2025 anyways. I guess we will find out.

Anyways, onto the numbers!

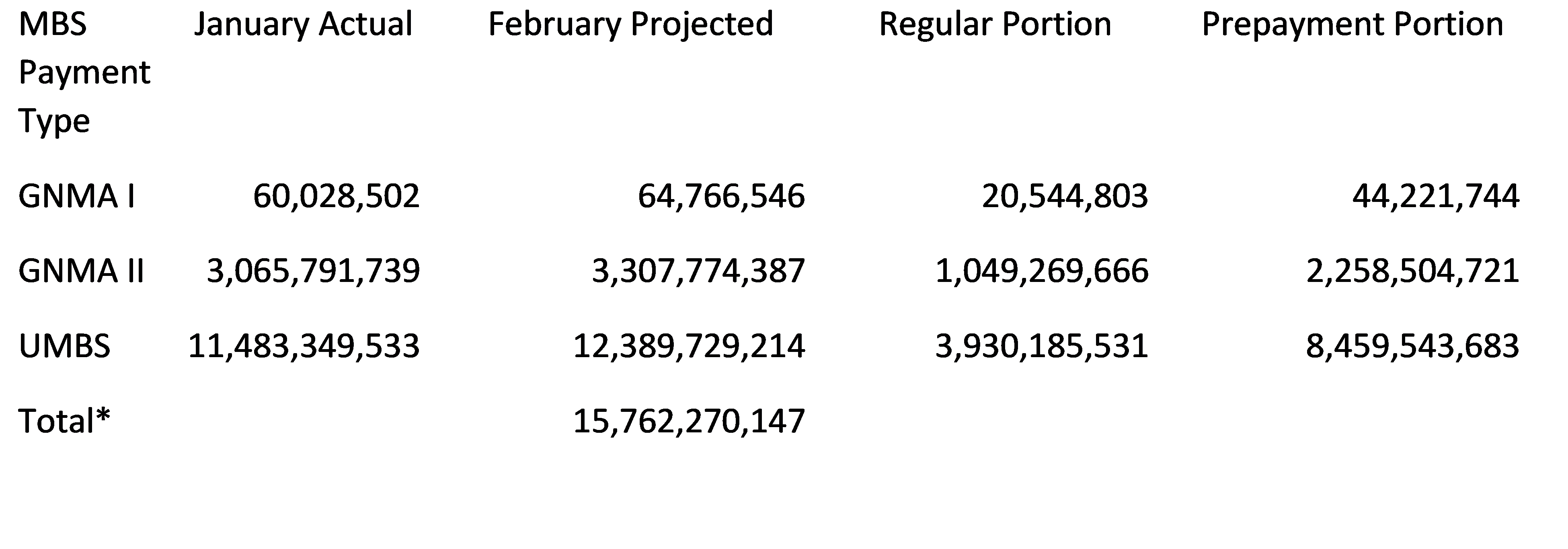

February MBS Payments

January prepayments were up some, rising ~12% vs December. Using @DharmaTrade ‘s scripts which faithfully apply the 112% multiplier only to the prepayment portion of each MBS payment, we reach the following MBS payment projections:

*Note an additional 15,000,000 in Fed held CMBS is also expected to rolloff bringing us to a total MBS rolloff of 15,777,270,147

February UST Rolloff

Fed coupons maturing in February are:

· Total notes/bonds: 77,341,976,800

· Total FRNS/TIPS: 0

· Total Coupons: 77,341,976,800

Since Coupons maturing exceed the 60b cap, the Fed will fully reinvest their bill maturities in February.

Between the mid month and end month maturities, the Fed rolls off an amount proportional to the total amount maturing. Accordingly, since 60b will be rolled off out of a total ~77.342 for the month. ~77.5775% (60/77.342) of the amounts maturing on 2/15 and 2/29 will roll off.

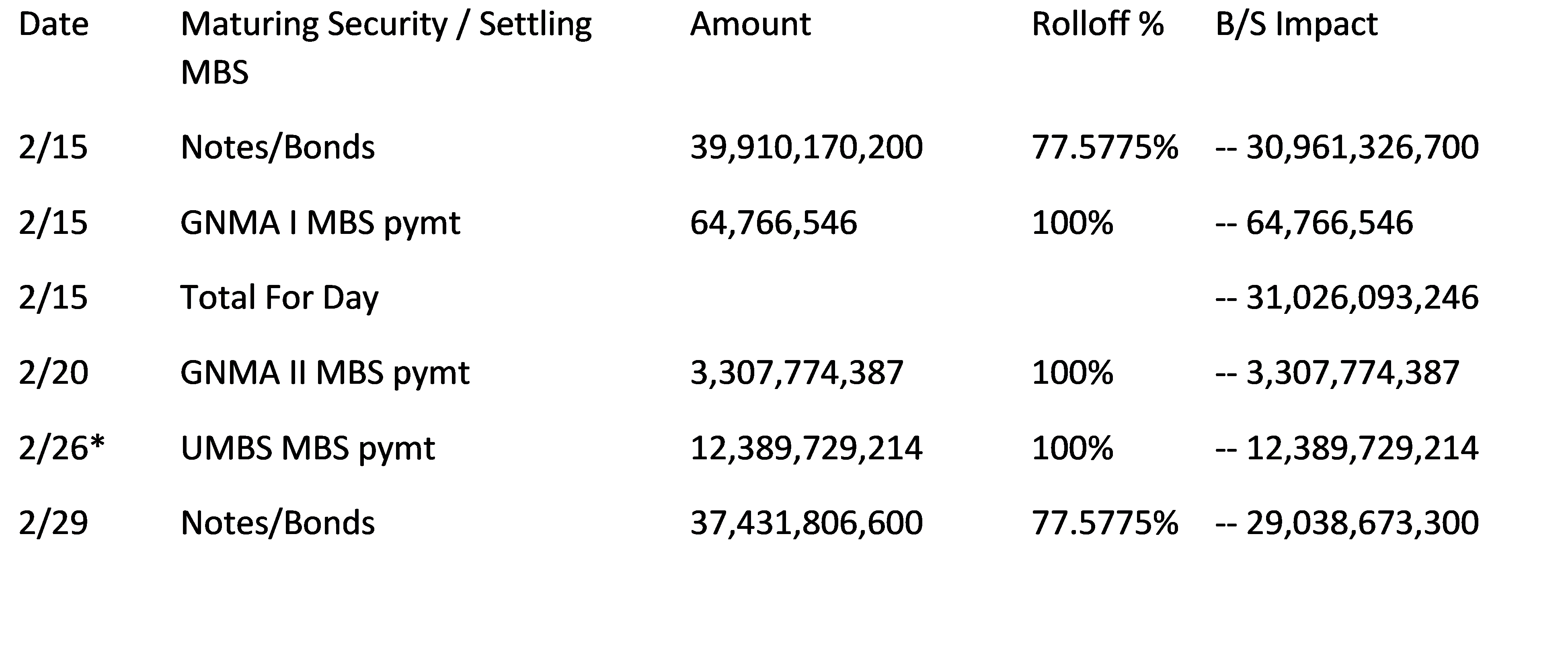

QT Balance Sheet Impact by Date in February

*The UMBS MBS payment due on Sunday 2/25 will instead be received on Monday 2/26.

Weekly Projections for February

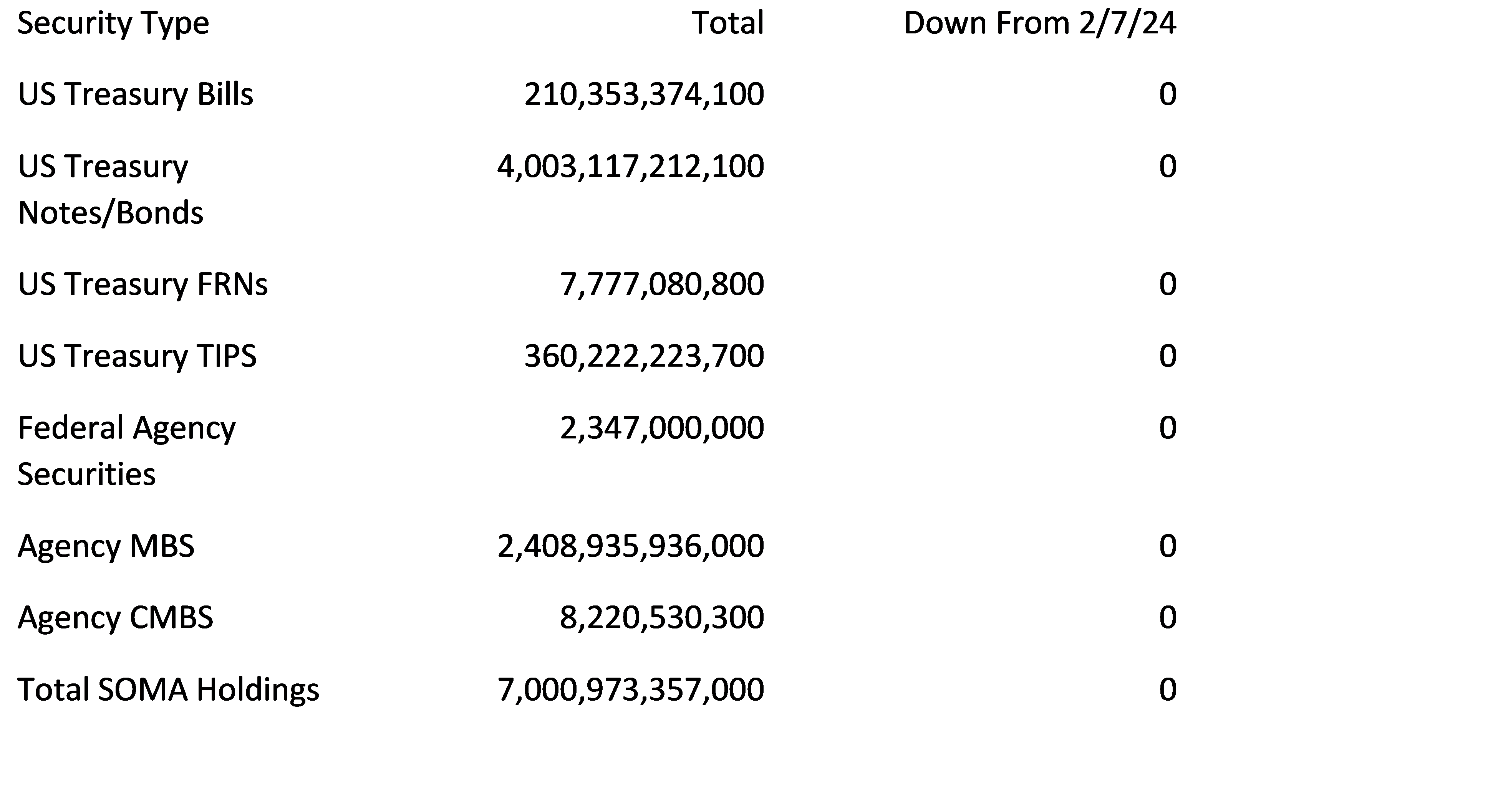

2/7/24 SOMA Domestic Security Holdings baseline

2/14/24 SOMA Domestic Security Holdings projection

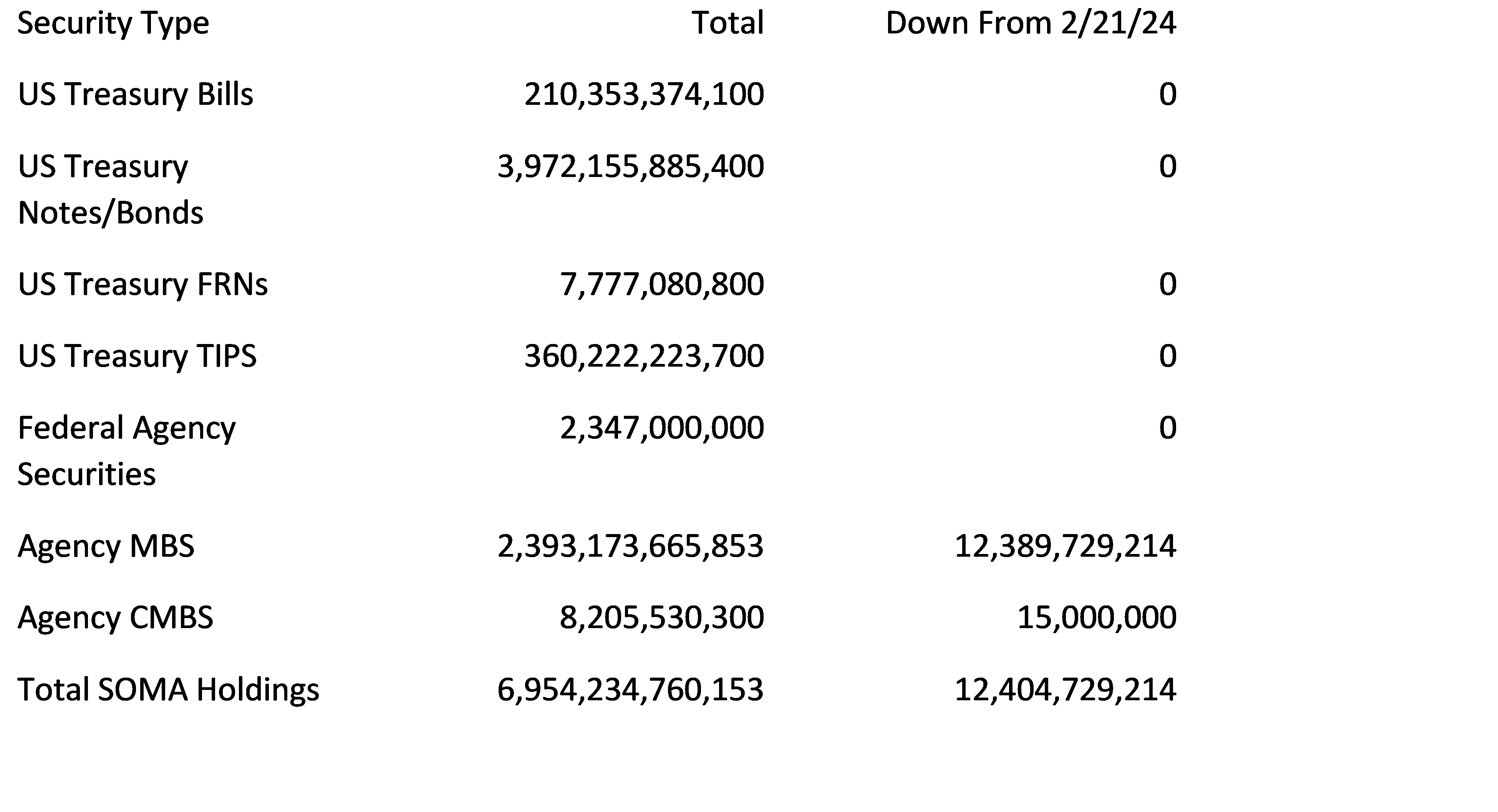

2/21/24 SOMA Domestic Security Holdings projection

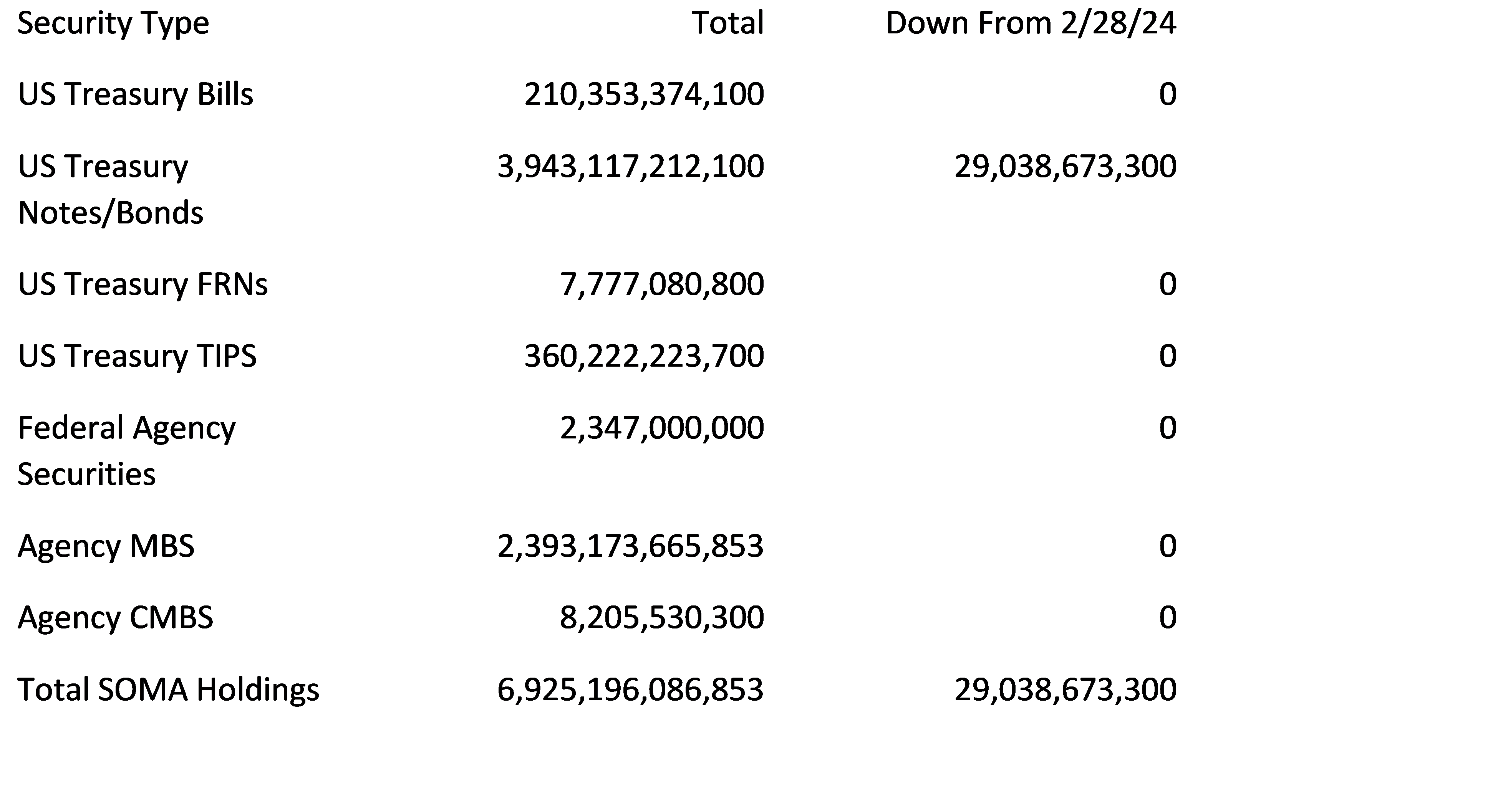

2/28/24 SOMA Domestic Security Holdings projection

3/7/24 SOMA Domestic Security Holdings projection

Add Ons

These posts detail QT from a rolloff perspective, but rolloff is really just reduced reinvestment that would otherwise be required to maintain the balance sheet level. Until June 2024 when UST QT will hit its first month it doesn’t hit the 60b cap across both bills and coupons, every month includes some reinvestment of bills, or bills and coupons. If you know (or can accurately project) the offering amounts, then these reinvestment (Fed Add Ons to auctions) amounts can be known in advance. The Projected Add Ons for February are below.

As always, thanks for reading.

Best,

John

Note for new readers – If this is your first time reading my posts on QT and are interested in the mechanics behind QT and how I reach these projections. Please see my earlier posts starting with Reverse Engineering QT on July 29, 2022.

Also, if you are interested previewing the scripts authored by @dharmatrade that leverage the FED APIs to pre-calculate QT treasury/bill runoff schedules and MBS payments for the upcoming month implementing the QT rules and MBS estimation methods described in this series of posts, reach out to him on twitter. His scripts are a huge help in putting these posts together.

Great analytical take as always, thank you, kudos to your work.

Have a great day!