Spring 26 QRA Wrapup and Treasury Model Update

Most of my projections leading into the Spring QRA matched what Treasury announced last week….. with one glaring exception.

First, the good…..

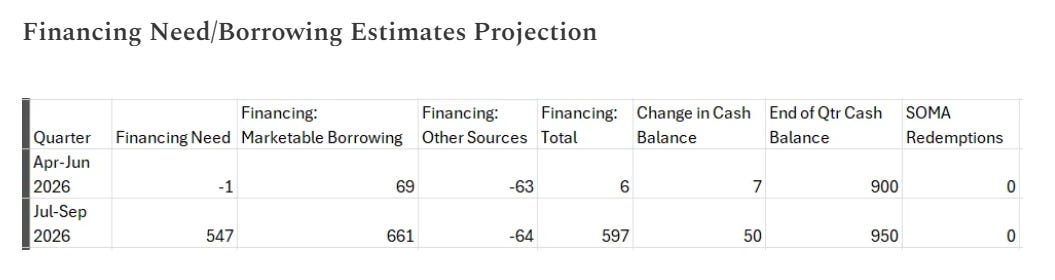

The Total Treasury Model (“TTM”) projected a Financing Need of 547b and Marketable Borrowing of 661b for the Jul-Sep qtr.

Treasury projected a Financing Need of 557b and Marketable Borrowing of 671b for the same qtr. That is fairly remarkable alignment this far out. As part of that Marketable Borrowing estimate, Treasury agreed that the most likely TGA level (rounded to the nearest 50b) at the close of business on Sept 30 is 950b, a rise from end of Junes 900b. Note that Im not just guessing that Treasury is going to raise the projected end of qtr balance (which again is not a target). The TTMs detail output tells me this is likely.

The image above is from the detailed TTM output released with last Sundays QRA projection post (the same output is included with every TTM update post). Note that the TGA End level the TTM projected for 9/30 was ~968b (orange highlight). Treasury always lists in 50b increments so I round that down to 950b and use that as my projected end of qtr level that Treasury will use in their QRA projections.

The daily projected TGA end level is an application of the days TGA cashflow (projected Daily Treasury Statement Table II deposits shown in column D minus withdrawals in Column E) the projected debt issuance/redemption shown in columns F and G, any Treasury buyback operations in column H and projected bill drop (the difference between the face value of treasury bills and the cash Treasury actually receives, e.g. Treasury may sell 100b in 4-week treasury bills but only receive 99b in cash for them, thus a 1b bill drop).

I also calculate the projected TGA risk policy level for that day and the projected cushion over it. I figure out likely bill issuance by iteratively running the model and tweaking bill increases/reductions to get the cushion over the risk policy high points mid months and end of month to be just a small amount (10-40b range ideally) for the extent of the model run.

Sometimes, it becomes clear that Treasury would have to dramatically alter bill issuance to hit a TGA risk policy high point. Since Treasury favors more stable and predictable bill issuance patterns, those setups are more likely to be met with a short term cash management bill as a patch to get over the high point.

I predicted one for the end of this month.

which Treasury confirmed they intend to do.

So in general. the TTM did very well this QRA cycle with one glaring exception

Apr-Jun

The TTM predicted a Financing need of -1b for the qtr.

Treasury, which had previously (winter QRA) been projecting an 8b Financing Need increased it by a whopping 114b to 123b.

The end of June is only 2 months away and the huge flows with the most room for error (the April tax receipts) are already in for both the TTM and Treasury’s model. Its a huge amount of short term disagreement which is even more striking when you consider the alignment over Jul-Sep. So what are the likely causes of this disagreement?

Possibility 1. Treasury is much more front loaded with when the tariff refunds will start cash flowing out of the TGA than the TTM has modeled. I mostly relied on the research of others like JPM on the likely schedule for when these refunds would flow out. Perhaps Treasury thinks they will go out much more quickly than what market consensus seemed to be. Through the first week of May there is no evidence of these refunds going out in the Daily Treasury Statement data, but if this is the explanation, I would not expect to start to see it until very late in May through June.

Possibility 2. Treasury is expecting considerably less non-withheld income in June due to the changes in the OBBBA. On further evaluation of the TTMs expectations I think the TTM was expecting 10b more than it should have for paper receipts in June given January’s performance for the non-withheld/Other category. Furthermore, through the first week of May the TTM was projecting about 10b more (almost all of it on the first of May) than actually came in. So it seems this would explain 20b of the 125b difference between Treasury and the TTM. We will just have to see how June plays out.

Possibility 3. Treasury expects Withholding to underperform trend growth over the next two months due to folks getting large tax refunds this year and subsequently adjusting their withholding amounts. Through the first week of May there is no evidence for that with withholding coming in just a smidge heavy vs. the TTMs expectations, but Ill keep watch on it.

Possibility 4. Treasury expects Iran war expenses start hitting in mass before the end of the quarter. I have no doubt there will eventually be a large bill due to Iran conflict expenses that will be paid via cashflow out of the TGA, and to some extent there already has been elevated spending out of the Dept of Defense (DoD) - misc, but those flows are not massive (5-7b/month that is already baked into the TTMs expectations). I also think large expenses like radar installation replacement etc. will take a fair amount of time to contract out and then eventually cashflow out of the TGA. Perhaps Treasury has a different opinion. Through the first week of May though potential Iran war expenses are actually lighter than the TTMs beefed up expectations for them. Ill keep watching

Possibility 5. Treasury expects some wildcard spending item like Federal Financing Bank to make some 50b withdrawal. This occasionally happens (and I am unaware how to project these) but we are pretty far removed from the SVB era cleanup which causes a few of these a few years ago so Im doubtful this will be the case. Anyways Ill keep watch.

Possibility 6. Treasury is just wrong. The TTM has outperformed Treasury’s models for 4 consecutive quarters and a number of them involved Treasury revising their initial estimate the wrong way.

The next two months will be interesting to watch and Ill keep yall posted on how this horse race develops.

Full TTM Output

For paying subscribers, the full updated TTM output through the end of the fiscal year is attached below the paywall.