March 24 QT

March 24 QT

Will Janet squash the mechanical taper in June?

TLDR

QT will reduce Fed balance sheet by ~75.3b in March: 60b for UST, 15.3b for MBS. UST coupon reduction is much heavier on the end of month maturities. There is 15.2b of bill rolloff this month

If the Treasury anoints the now regular Thursday 42 day cash management bill to benchmark (6w) status before May 1st, the full 60b cap for UST will roll off in June with no change in the rollover mechanics

Greetings!

Last month I detailed why QT would mechanically “taper” in the months of June, September, and December this year if the Fed did nothing to change the rollover mechanics. (and with inertia still occupying the top slot in powerful forces in the universe I think that must be the base case) But there is a not that unlikely wildcard out there that would allow the Fed to hit the full June cap (and likely also September and December or at least very close) with no change in the longstanding rollover mechanics. That wildcard? ….. <Janet enters the chat> … Treasury could elevate to benchmark status the 42day cash management bill that they have been regularly issuing in size every Thursday since the resolution of the debt ceiling impasse. The last 2 QRAs have mentioned that this was being evaluated and the tone of the language used implied to me that it was probably more a matter of when not if that benchmarking happens.

So why does that impact the pace of QT and allow the Fed to hit the rolloff cap for Treasuries of 60b in June? De facto, the Fed does not reinvest in cash management bills. There doesn’t seem to be anything explicitly stated in the Treasury rollover policy that they wont, but the data to this point is clear. They don’t. I assume they don’t for good reason due to the potential variability of those bills. For example, Cash management bills don’t necessarily have to mature on a day when the Treasury has regularly scheduled issuance (like for example cusip 912797MF1 which matured on Monday June 5th last June in the peak of the debt ceiling impasse). In theory that could leave the Fed in the position of having maturing funds it wants to reinvest in treasuries and no new treasuries issuing that day. Not that the Fed couldn’t deal with that situation in a one-off way, but its much simpler and cleaner to just stick to the benchmarks that have predictable and correlated issuance and maturity schedules. Thus far, that’s exactly what the Fed has done. Could they change it given how predictable and correlated with the Thursday issuance/maturity schedule the 42d CMB has become and decide to add it to the mix in the absence of a benchmark? Sure, I just think with inertia and all that they are unlikely to do that, even to avoid the “missing the cap” questions that might arise when they miss it in June.

On the other hand, If Treasury elevates the 42d CMB to 6w benchmark status I fully expect the Fed to start reinvesting into that tenor soon after the benchmark status is established. I don’t think the Fed would even consider it a change in policy, just the existing rollover policy reacting to the addition of a new benchmark bill.

So what happens if the Fed starts reinvesting in these 42d/6w bills? It opens up an avenue for bills that are reinvested in during months with higher coupon maturities like May (and thus more bill reinvestment) to mature in months with fewer coupon maturities instead of just 3 or 6 months later in months with again high coupon maturities like August, breaking the trap I described last month.

Looking forward to May, the Total Treasury model projects the following total bills held by the Fed will be maturing each date.

On Thursday May 2nd, 9th, and 16th combined approximately 46b of bills will mature. Each Thursday the 42d/6w bill constitutes about 1/3 of the issuance that day, so the Fed would accordingly reinvest about 15b or so in bills that would mature on June 13th,20th, and 27th, thus giving June enough maturing bills to cover the current ~12b gap. I haven’t had enough time to modify an alternate version of the Total Treasury Model to reinvest in these bills to see whether it would allow September and December to hit cap, but even if it isn’t quite enough, it will get much closer to hitting the caps those months.

So end of the day Treasury benchmarking the 42d bill (or fed just choosing to reinvest in the 42d cmb) mostly solves the feds “mechanical taper” issue in June and possibly September and December. We will just have to wait and see if it happens.

Anyways, onto the numbers!

March MBS Payments

February prepayments were up, rising ~15% vs January. Using @DharmaTrade ‘s scripts which faithfully apply the 115% multiplier only to the prepayment portion of each MBS payment, we reach the following MBS payment projections:

*Note an additional 10,000,000 in Fed held CMBS is also expected to rolloff bringing us to a total MBS rolloff of 15,252,236,387.83

March UST Rolloff

Fed coupons maturing in March are:

· Total notes/bonds: 44,789,553,000

· Total FRNS/TIPS: 0

· Total Coupons: 44,789,553,000

Coupons will fall short of the 60b cap in March and accordingly there will be 15,210,447,000 rolloff of bills as well. The Fed does this proportionally to the amount of bills maturing each Tue/Thur. For March, the rolloff percentage for bills is a whopping ~ 80.8105%. This is calculated by 15,210,447,000 (total bills to rolloff) / 18,822,360,000 (total bills maturing).

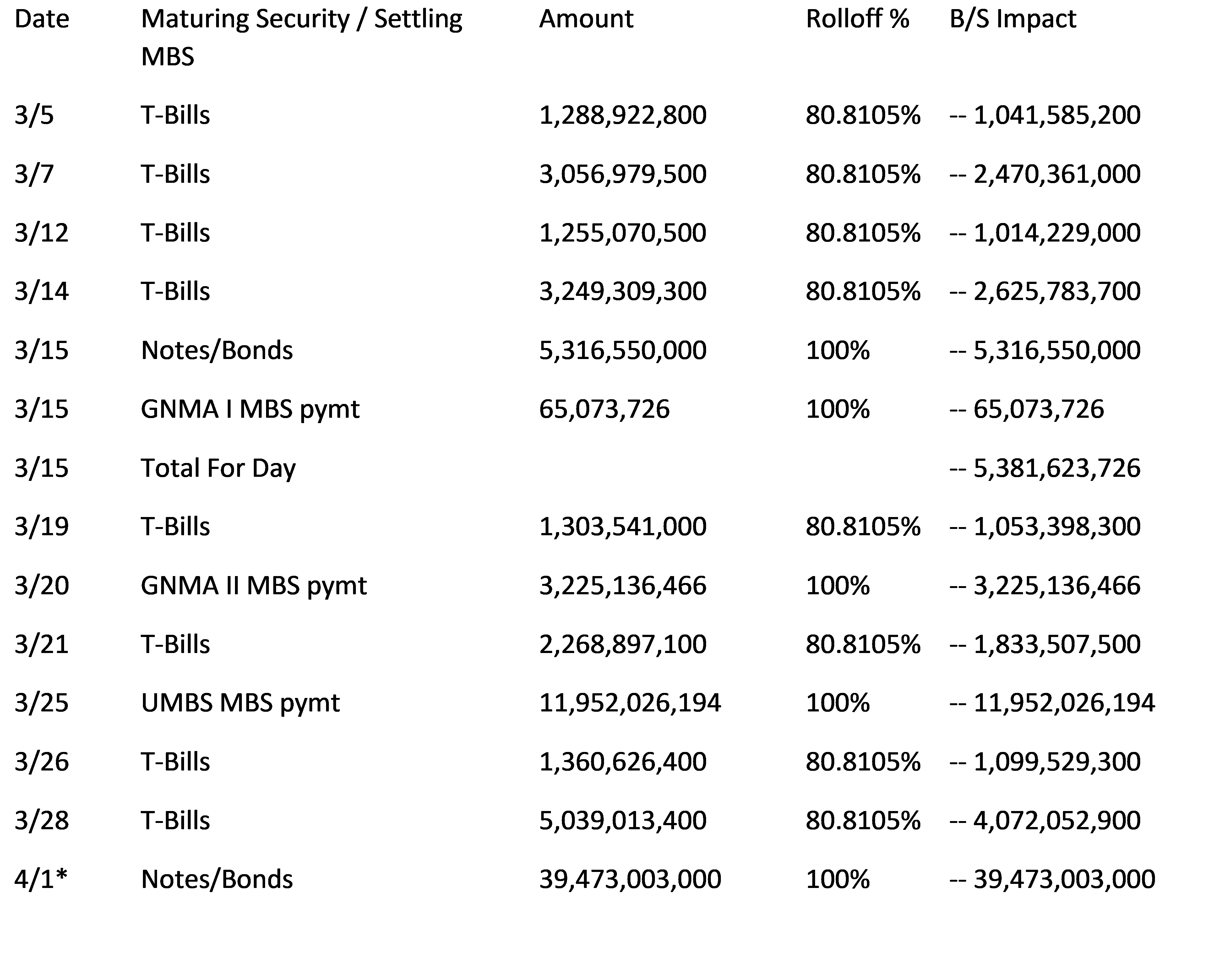

QT Balance Sheet Impact by Date in March

*The Notes and Bonds maturing on 3/31 will be settled on 4/1

Weekly Projections for March

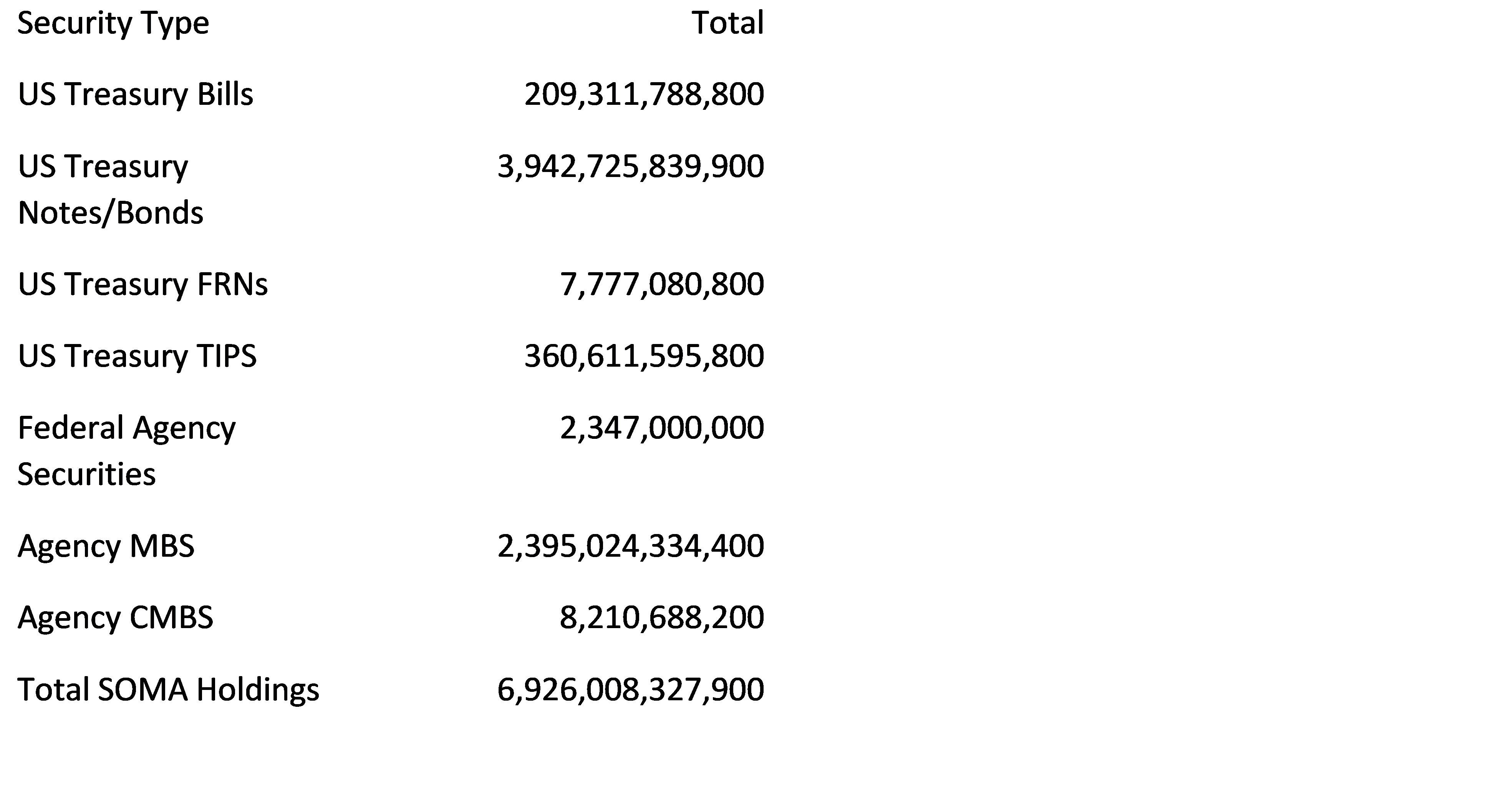

3/6/24 SOMA Domestic Security Holdings baseline

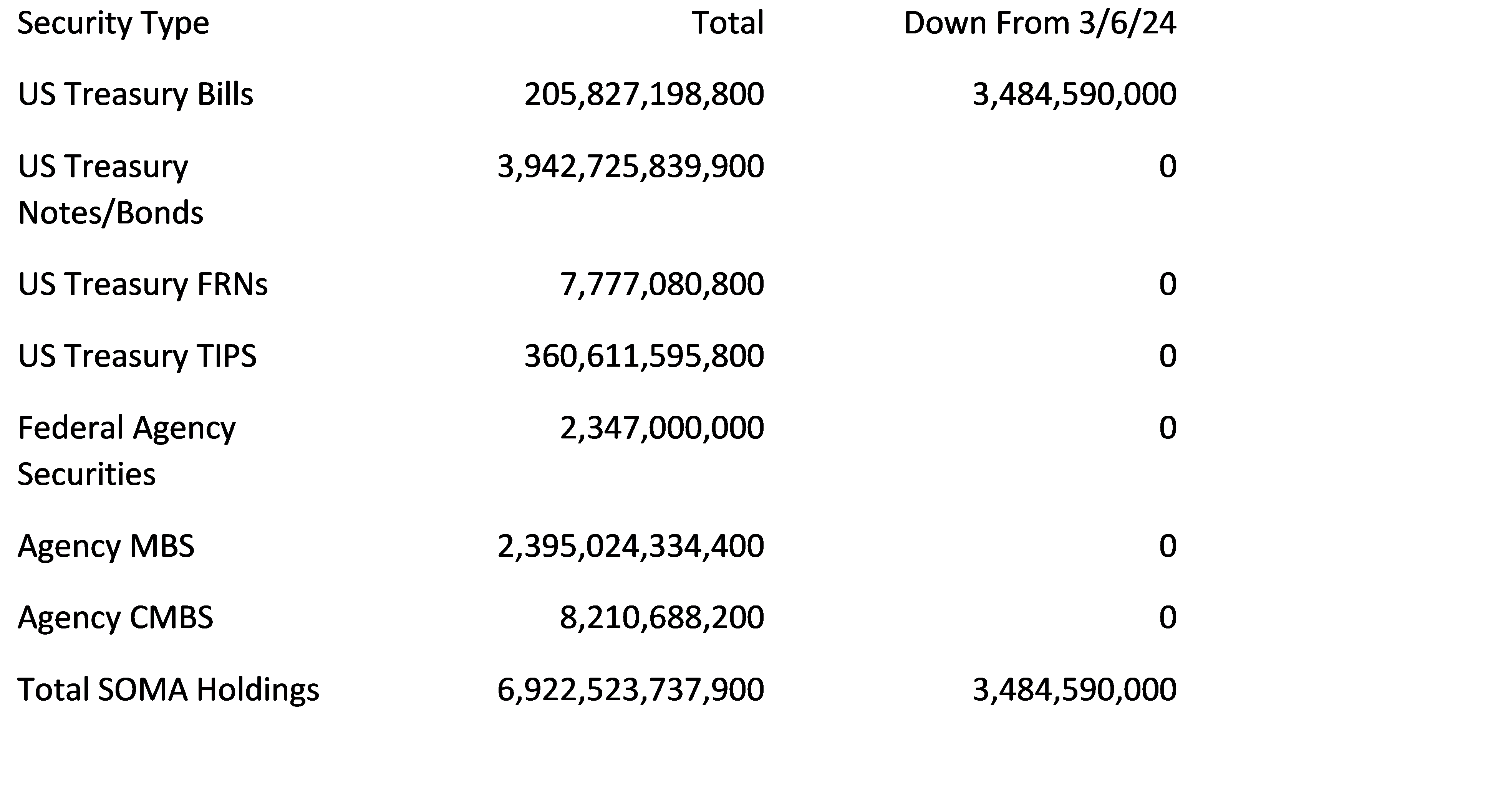

3/13/24 SOMA Domestic Security Holdings projection

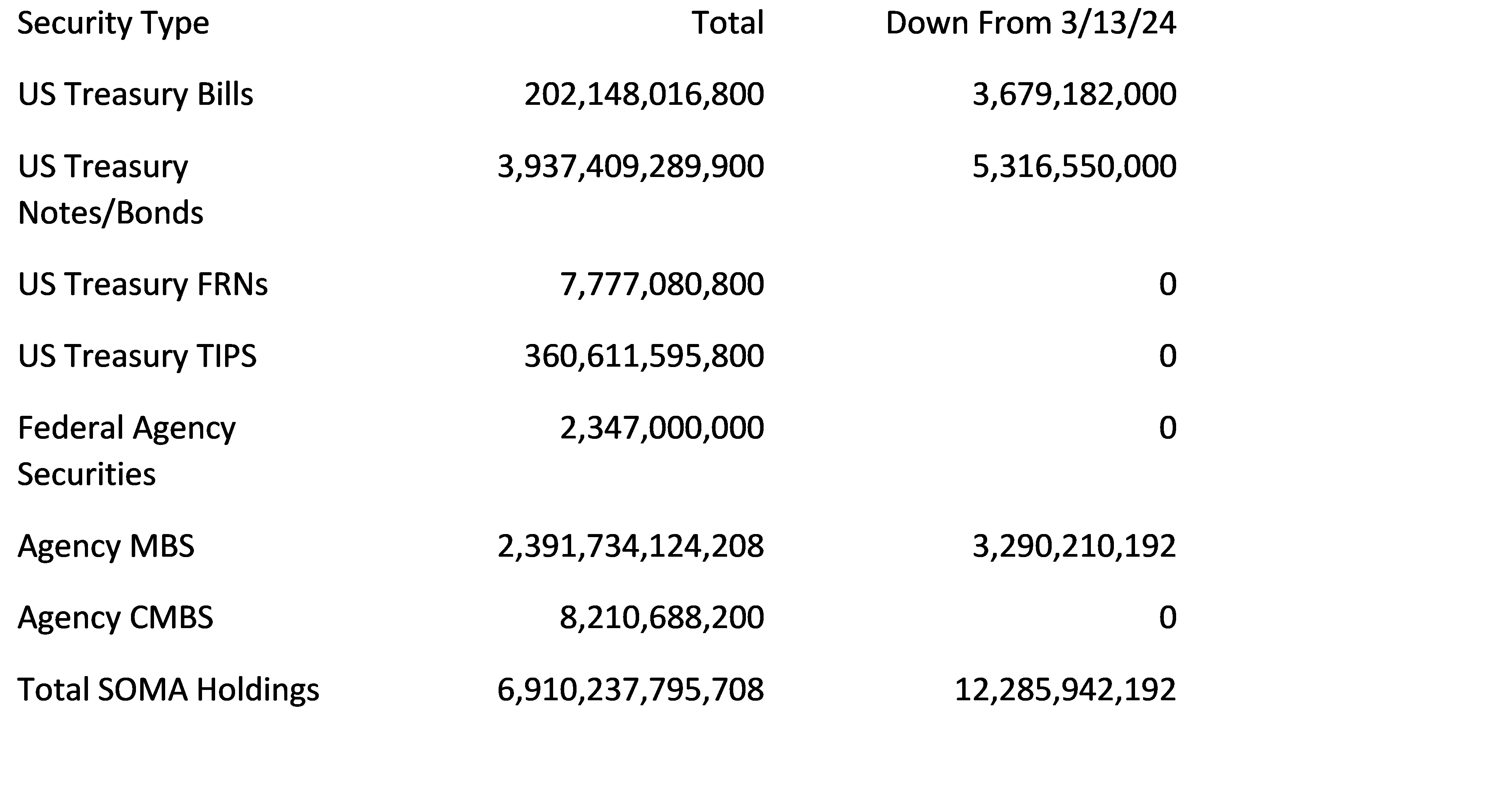

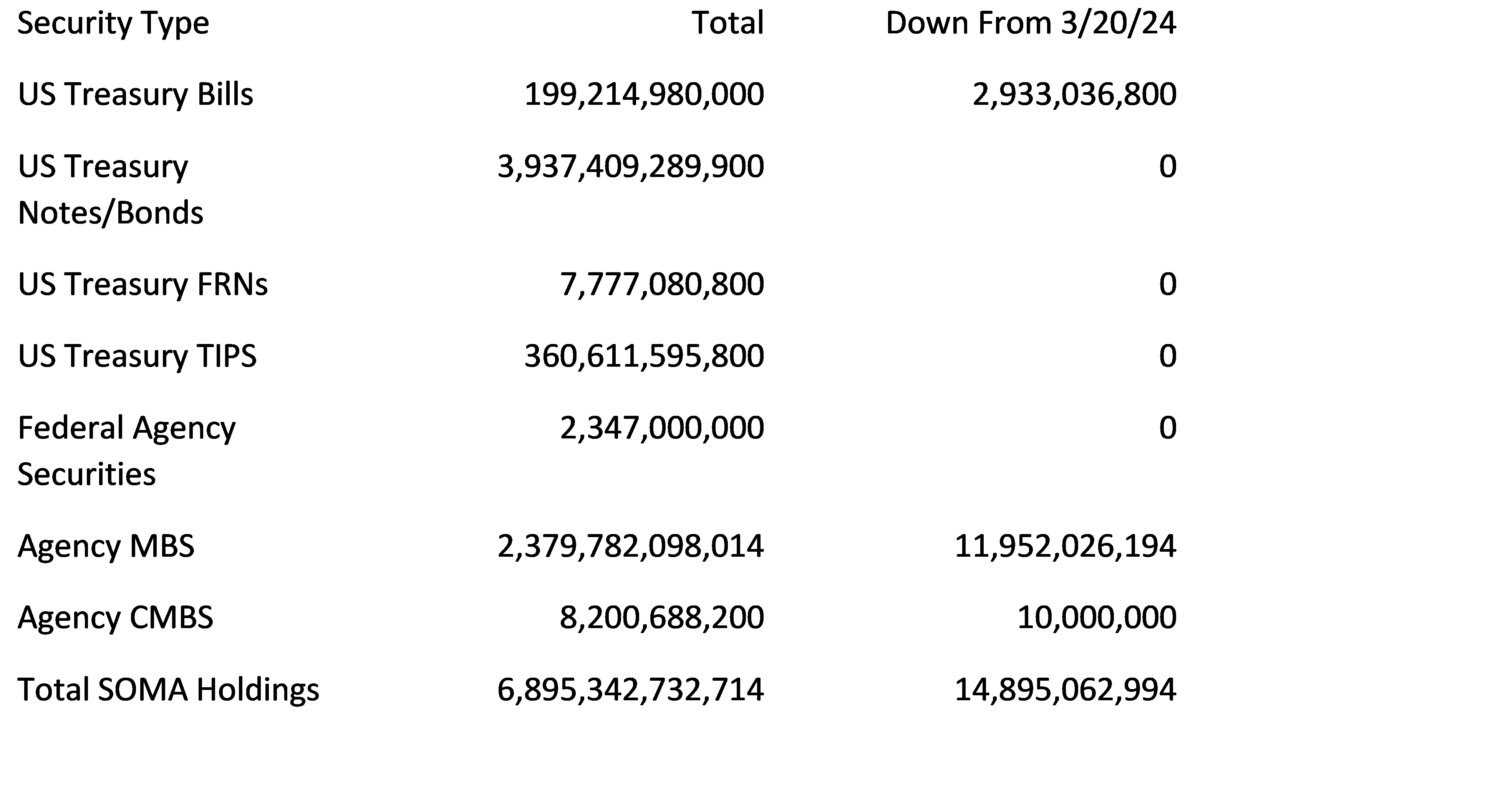

3/20/24 SOMA Domestic Security Holdings projection

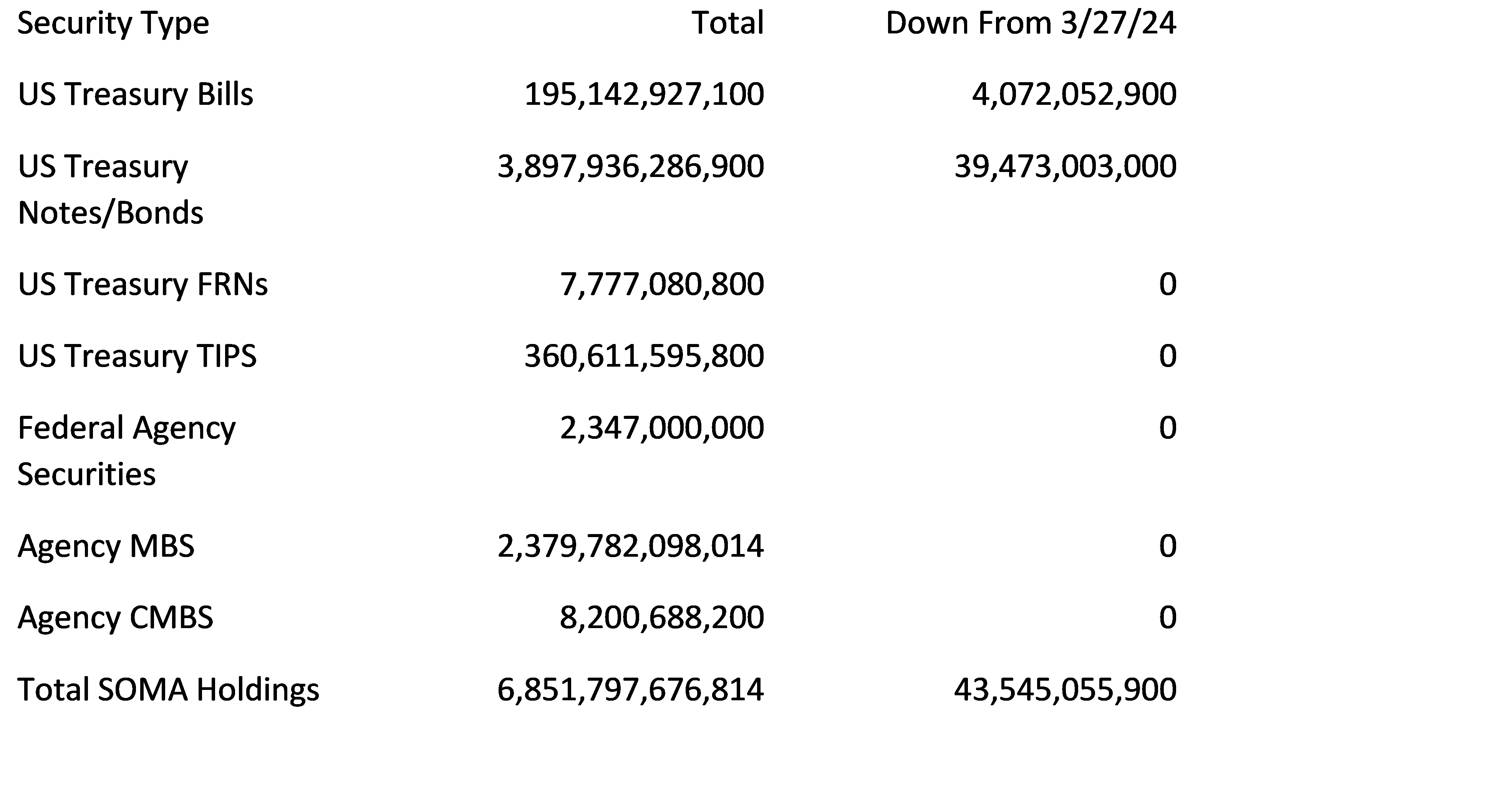

3/27/24 SOMA Domestic Security Holdings projection

4/3/24 SOMA Domestic Security Holdings projection

Add Ons

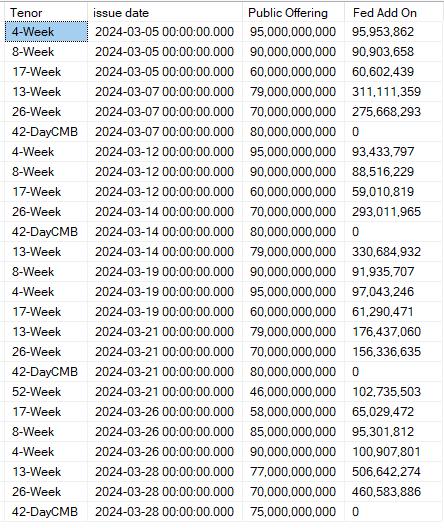

These posts detail QT from a rolloff perspective, but rolloff is really just reduced reinvestment that would otherwise be required to maintain the balance sheet level. Until June 2024 when UST QT will hit its first month it doesn’t hit the 60b cap across both bills and coupons, every month includes some reinvestment of bills, or bills and coupons. If you know (or can accurately project) the offering amounts, then these reinvestment (Fed Add Ons to auctions) amounts can be known in advance. The Projected Add Ons for March are below.

As always, thanks for reading.

Best,

John

Note for new readers – If this is your first time reading my posts on QT and are interested in the mechanics behind QT and how I reach these projections. Please see my earlier posts starting with Reverse Engineering QT on July 29, 2022.

Also, if you are interested previewing the scripts authored by @dharmatrade that leverage the FED APIs to pre-calculate QT treasury/bill runoff schedules and MBS payments for the upcoming month implementing the QT rules and MBS estimation methods described in this series of posts, reach out to him on twitter. His scripts are a huge help in putting these posts together.

John, Isn’t the sum of all the 42day CMBs outstanding currently about $550 Billion ? Treasury’s significant increase in Bills vs. Coupons last year “the show must go on” to suppress LT rates, or else :) That along with Treasury’s decision to greatly expand 2s, 5s vs. 10s & 30s. Benchmarking of another sort, LT prices/rates :)

Maybe next post you can delve into “The New Neutral” :)

Maybe Fed will use June as timely starting date to slow pace of QT matching declining runoff maturities you note.

great take John, thank you!