Detailed October QT

TLDR

B/S will rolloff by ~78.2b in October. MBS payments should be ~21.4b in October. Subtracting 3.2b for the last bit of previously purchased MBS to settle and we get 60 (UST) + (21.4 – 3.2) (MBS) = ~78.2b of total B/S rolloff in October.

**Note for new readers – If this is your first time reading my posts on QT and are interested in the mechanics behind QT and how I reach these projections. Please see my earlier posts starting with Reverse Engineering QT on July 29.

Hello again!

FNMA Benchmark CPR numbers (prepayment rates in September for FNMA and FHLMC loans) came out yesterday enabling me to project what the MBS payments will be for October and accordingly, do a detailed look at QT for October. This article continues to project B/S runoff on a weekly basis so the projections can be compared to SOMA actuals when the B/S is released on Thursday afternoons ~4:30EST. That said, the actual liquidity impact of the components of B/S decline (or as seen occasionally in previous months B/S rise) do not occur on the Thursday the B/S is released. Rather they occur sometime from the previous Thursday to the Wednesday the B/S is effective for. If your interest in QT is coarse, that shouldn’t matter, but with growing interest in net liquidity as a predictor for S&P 500 performance (see @maxjanderson pinned thread) I thought the additional detail of day of liquidity impact would be appreciated by some readers.

October MBS Payments

MBS payments for the month should be ~21.4b. This payment projection is based on FNMA and FHLMC prepayment rates being ~87% for September vs. August. Accordingly, we should see a similar drop in MBS payments. This methodology proved fairly accurate for the UMBS payments last month so I have a fair degree of confidence it will be close again this month.

Detailed MBS payment projections are

UMBS: 16,668,812,000 (last month actual) * .871 (ratio of September CPR to Aug CPR for FNMA and FHLMC loans) = 14,513,854,284 UMBS

GNMA I + GOLD : 2,036,297,000 (last month actual based on 25% of GNMA I + GOLD + GNMA II) * .85 (applying a bit more of a discount based on a lower than expected GNMA I + GOLD + GNMA II payment last month) = 1,730,852,450

GNMA II: 6,108,891,000 (last month actual based on 75% of GNMA I + GOLD + GNMA II) *.85 = 5,192,557,350

Total Projected Oct MBS: 21,437,264,084

October UST Rolloff

Total notes/bonds: 43,614,523,000

Total FRNS: 2,758,435,100

Total Coupons: 46,372,958,100

Since Coupons maturing are less than 60b, the Fed will have to allow 13,627,041,900 of bills to rolloff as well this month. As discussed last month, the Fed does this proportionally to the amount of bills maturing each week. For October the rolloff percertage for bills ~ 16.5%. This is calculated by 13,627,041,900 (total bills to rolloff) / 82,356,773,900 (total bills maturing). Note that I erred high on the bill rolloff % when I calculated the 10/4 bill rolloff for the 10/5 B/S. This was due to me missing a 4 week bill that had yet to be issued and part of the Feds B/S, so my denominator was a little lower meaning higher rolloff %. This error is the cause of my small miss in the B/S for UST last week.

CMBS

I projected CMBS payments this month as well. They seem to follow a pattern of 1/6 of total CMBS payments received on the 15th and 5/6 of total CMBS payments received on the 25th. I took the avg total payments over the last two months for a roughly 45,000,000 expected total payment this month. Close to a rounding error honestly but better than no projection at all.

QT Liquidity Impact by Date in October

*Note that Treasuries maturing on Saturday the 15th and the GNMA I + FHLMC GOLD MBS payments due on the 15th are instead received the next business day which is Monday the 17th.

Weekly Projections through the end of October

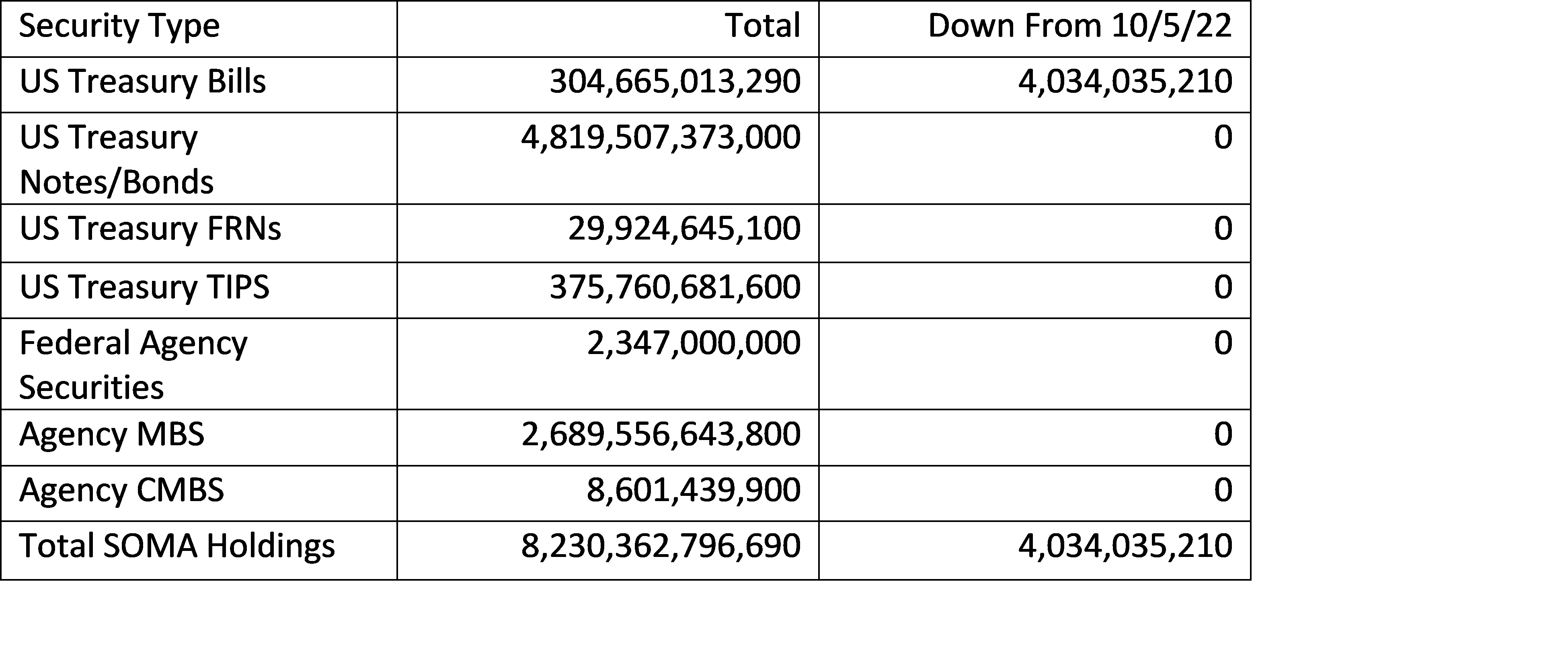

10/12/22 SOMA Domestic Security Holdings projection

10/19/22 SOMA Domestic Security Holdings projection

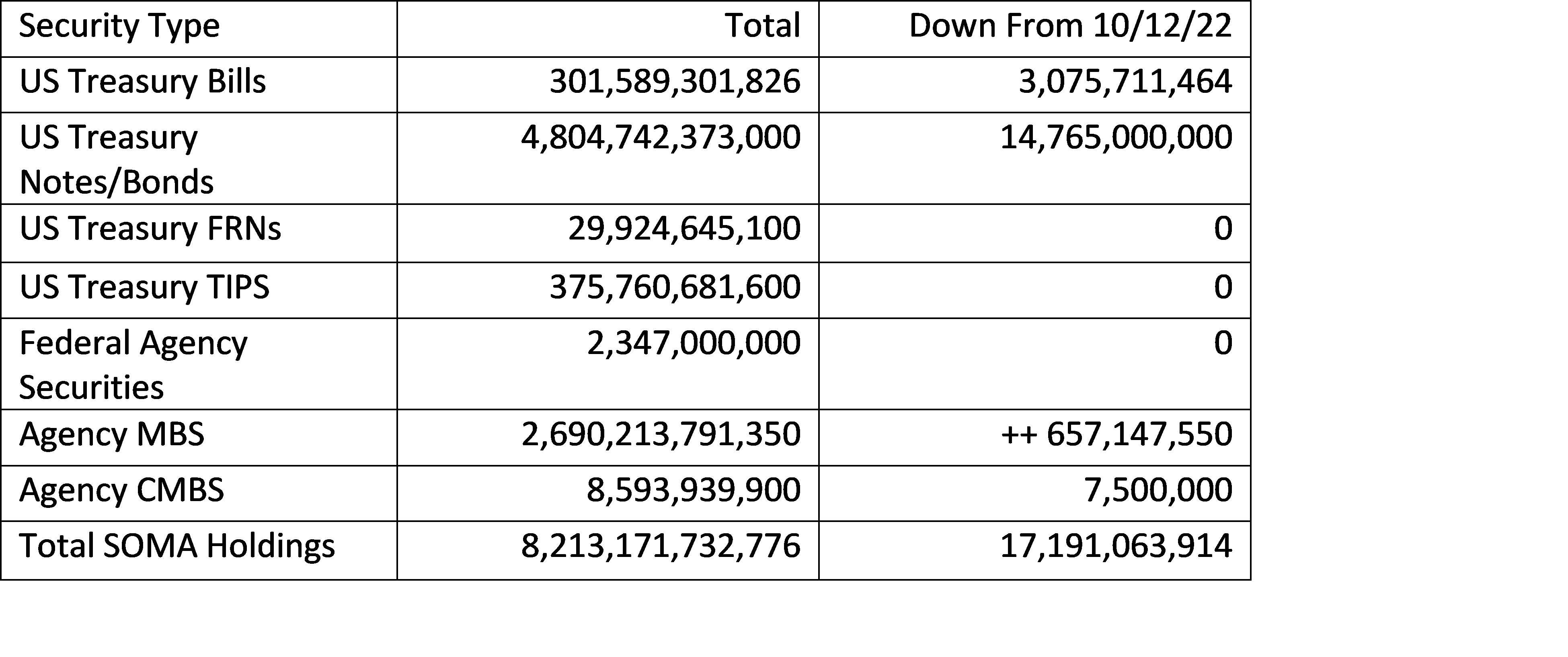

10/26/22 SOMA Domestic Security Holdings projection

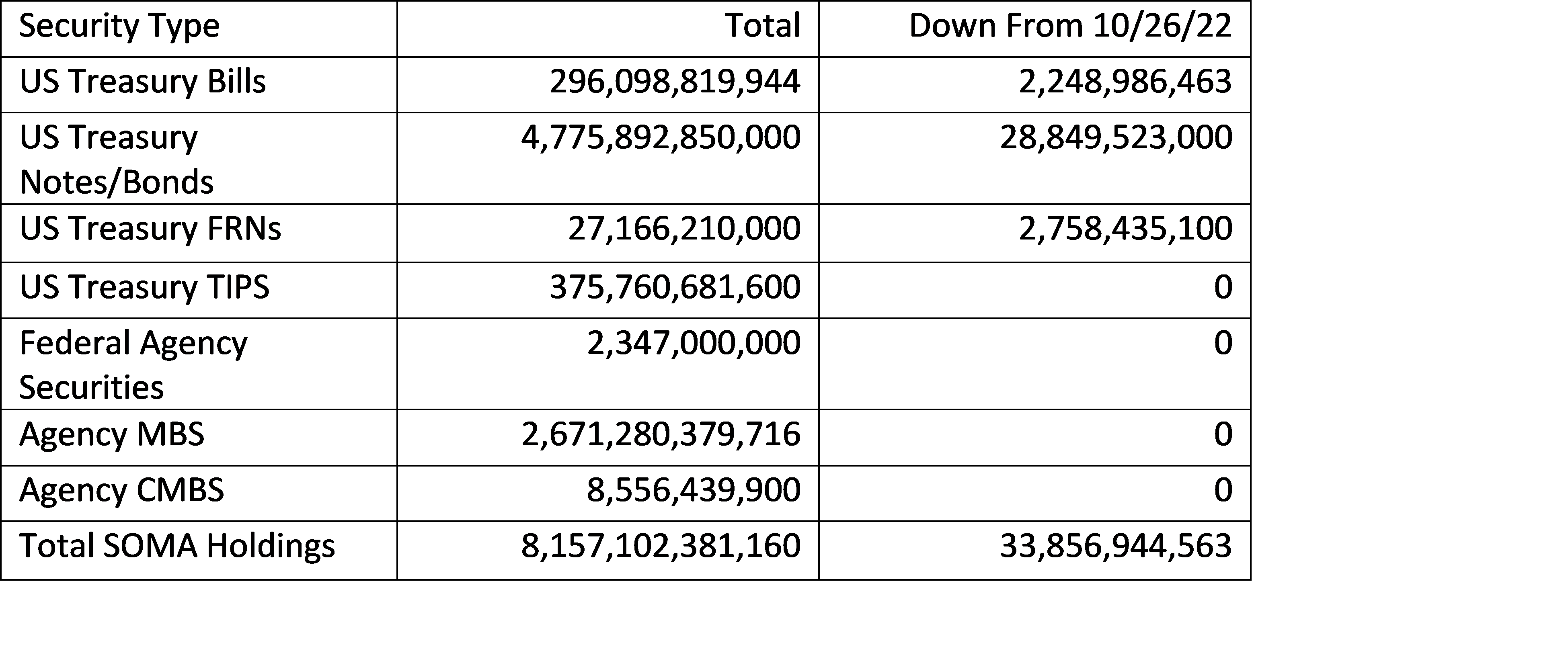

11/02/22 SOMA Domestic Security Holdings projection

Unless the Fed alters it, QT gets even more vanilla over the next half year or so since coupon maturity will exceed 60b (so no bill rolloff) and unless the Fed unexpectedly rolls any of the 3.2bish of MBS settling this month to November, all previously purchased MBS will have settled (so no more lagging MBS discussion will be needed).

Once again, thanks for reading.

Best,

John