April FHA MBS Data and another wrinkle to the coming storm

There is a large storm brewing in FHA mortgages that will start to hit at the end of the year and intensify into 2026. The FHA has pulled forward the start date for the new loss mitigation procedures to Oct 1. These new procedures will end the FHAs effectively unlimited and unending covering of borrower missed payments and require borrowers to actually make mortgage payments again. Those who were gaming the system will have to stop. Those who cant make those payments (or a 25% reduced version of them) will be forced to sell or face foreclosure. This has been well documented in this substack and elsewhere, but that reckoning is at least 5 months away, so not yet.

The Partial Claim Nonsense Continues for now

34392 partial claims were paid in the month of April. ~1500 fewer than March but covering ~2000 more payments.

16222 out of the 34392 (47%) were repeat recipients with 6680 (19.4%) on their 3rd or more partial claim. 10086 received at least one other partial claim since January of 2024.

Throw in another 7086 loans that were removed from MBS pools (almost certainly to be modified)

and that is over 41,000 loans in April that were cured (and thus removed from the SDLQ rates) due to loss mitigation efforts.

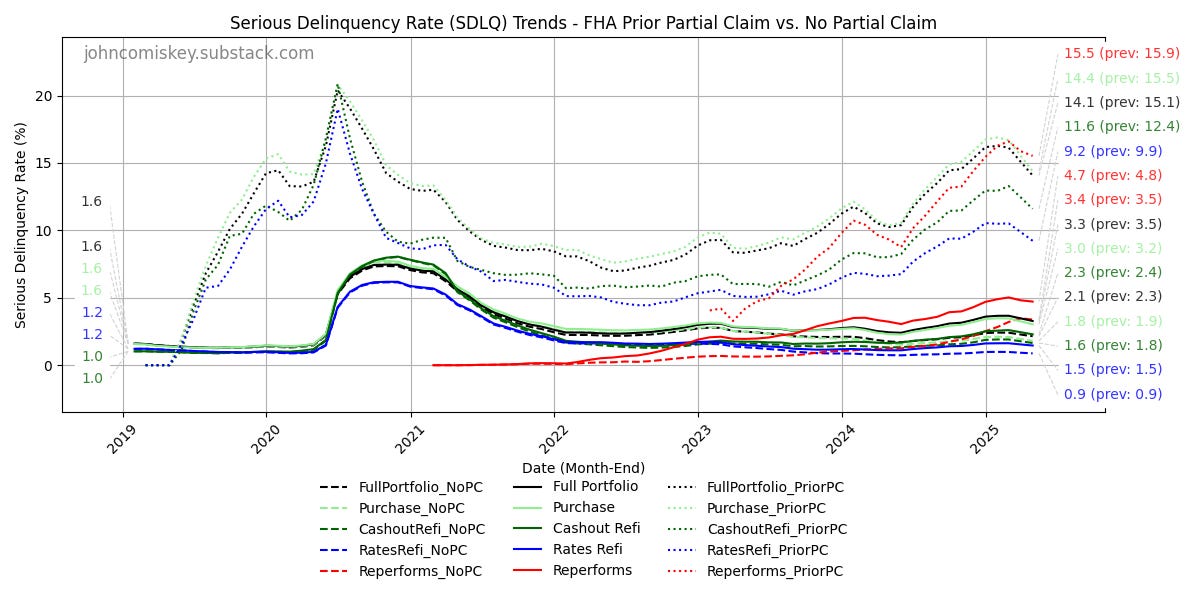

The redefault rates on loans that have received a partial claim in their past run 5-7x worse than loans that have not received a past partial claim.

But notwithstanding those dramatically higher redefault rates and even worse redefault rates for recent modifications, Loss Mitigation efforts absolutely do prevent forced selling/foreclosures in the majority of cases. but ONLY if Loss mitigation home retention options are available to the borrower and for a chunk of FHA borrowers that will stop being true in the not too distant future.

Who are these borrowers for whom Loss Mitigation home retention options will cease being available?

Keep reading with a 7-day free trial

Subscribe to Reverse Engineering Finance to keep reading this post and get 7 days of free access to the full post archives.